| WILSHIRE-THORNE RESIDENTIAL MORTGAGE | |||

| |

FAQ

Unhappy, tell me and I will forward the loan file to another lender free of charge. Also, you get a free copy of your credit and appraisal!! And best of all, you get a live person to talk with, from 7am-10pm. Check the internet or call Greg directly for the status of your loan, and details of what is remaining before you have your money. Ask for an email, fax or mail, or approval to be reassured and any other pertinent information.

|

|

||||||||||||||||||||||||||||

|

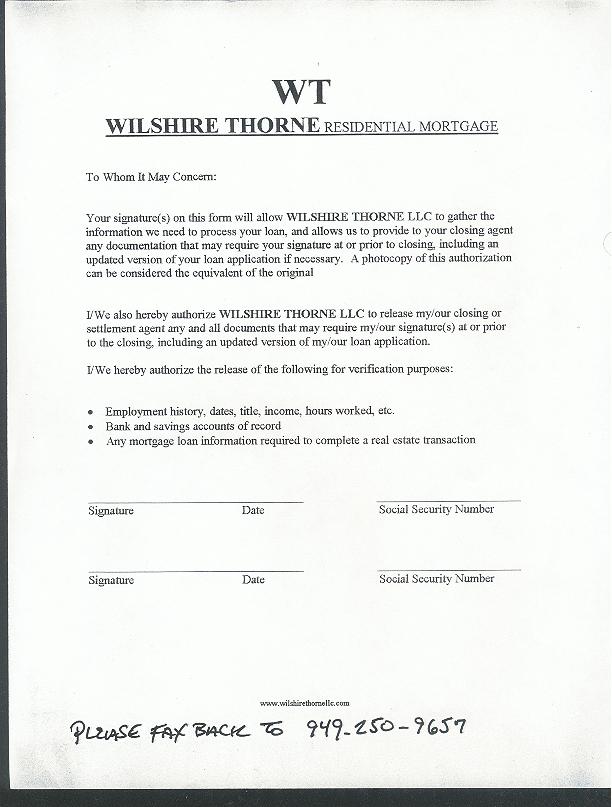

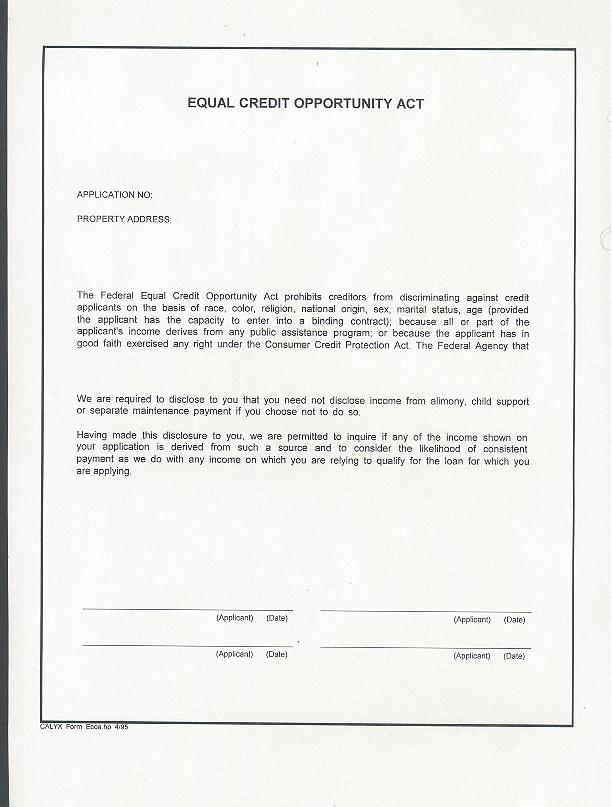

Disclosures-explanation, and printable forms, Click below, and then go to File/Print, on your browser. ..........Authorization Form - to get you the quotes based on good information,not guesses. ..........Anti-Discrimination Form - to prevent it and let you know your rights ..........Equal Credit Form - your rights Greg Fax- fax of what is needed to get reliable quote, in Microsoft Word97, format Why work with a smaller company? - Fixing Credit- improve scores, better rates, and payments Credit Basics- has the three bureaus, how they work, nice explanation. Credit Basics 2 - how they come up with the score Purchasing Disclosures, and developers fixing problems after purchase, information FINANCE LINKS Yahoo.com, finance, great place to check the rates, add about 1.5% to the 10 year bond rate for the 30 year fixed. Remember the Fed doesn't directly affect the fixed rate. It is largely determined by the buying and selling of 2 , 5, and 10 year bonds. The market for these is the Chicago Board of Trade. Why is this important? Well, it changes constantly all day long, from 8 am to 3 pm, approximately. It goes up and down and is dependent on a free market system. Not the Federal Reserve. Federal Reserve maneuvers affect Variable Rate Mortgages and Credit Cards and Equity lines. Products by which the rate varies depending on the prime rate. 15 Year fixed rate mortgages are about .5% less than the rate for 30 yr. Fixed products. Yahoo has some great links, and also good for investing.

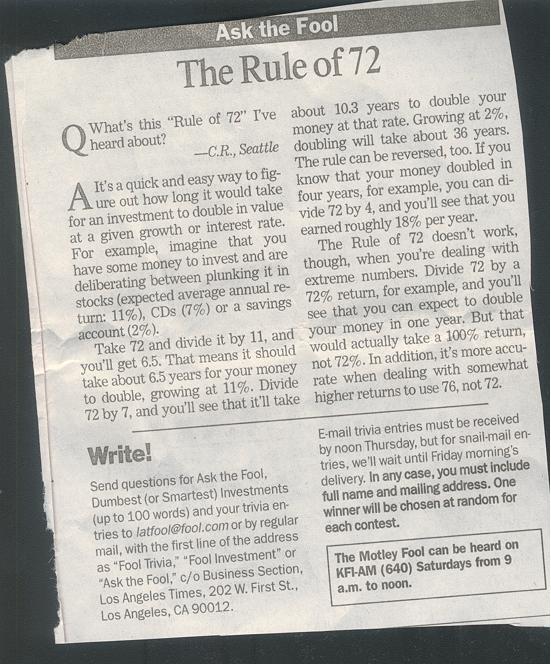

Realtors- good link on the role and legal obligations 10 Things Lenders won't tell you Ten Year Bond, Add Approximately 1.5% to it for 30 Year Fixed Rate, Subtract .5% from that for 15 Year Fixed Rate 10 Year Bond In 1960's Territory, Mortgages, 40 Yr Low, Aug.2002 Rule of 72, Rate of Return Equation- very simple way to figure the benefit of investments Trusting Your Financial Manager - vitally important!! Excellent article. IRS, Points and Allowed Deduction- Big deduction when refinancing from old Mortgage. New mortgage only when paid which is 1/30'th per year. Keep your Settlement statement and Loan Note, and Trust Deed, copy onto computer and put in safe place. Refinancing, Benefits of- $150/month, 20 years, @ 8%/year rate of return = $88,000.00, 30 years= $223,000.00; $250,8%,20yr,=$147,000.00, 30 yr.=$372,000.00. Live Wealthy, When Wealthy- A $20 today could be $396, 30 years from now. **Assumes 10% rate of return, 30 year term and a one time amount of $20. Steps Illustrated Clearly, or What to expect, and how to prepare!! 10 Year Bond, 1 Year chart, August 2001-2002, fixed rate comparison, November 2001, low beaten in August 2002, 3.9%, This is a great index to use to gauge 30 Yr. Fixed rates and 15 Fixed rates. Adjustables are most effected by the Federal reserve. The 10 year bond is a good tool to tell what rates are doing in the fixed marketplace. Notice how the rates spiked up just into Nov. 2001. And how in July and August the major decline. The 30 yr. fixed hit a 40 year low of 5.75 % at par, as low as 5.375 obtainable. Unbelievable!! But notice how fast it went up in a matter of 3 days. Lenders are charging 2 points just to go to 1/8 jump from 5.875 to 5.75 or 5.75 to 5.625, incredible 2 points for a 1/8 th better rate.

FTC, Abusive Practices, a wonderful site, especially the link to "Need a Loan? Think Twice About Using Your Home as Collateral". Details on how to discover unscrupulous practices and to avoid them. Free Credit Analysis- Call Greg to run a credit and be on a list every 6 months, to be updated, scores given, and copies faxed, if allowed.

Free Report- Save $1000,s!!! That is THOUSANDS!!! Never before revealed information regarding fees, pricing, kickbacks, rebates, and other tricks lenders, brokers, banks and individuals play against the public. Email me and I will send out the file. Send to- gt@gregtaddeo.com, Twenty minutes to read, and it will give you the edge. Know this and you will run the show. Information is key!! Who knows how they make money? What are points and how do you really know how much a lender makes? What good is a Good Faith Estimate? Not much if you want to really know!! Why can a loan change in price ? Who is the person that really decides on your loan? The Loan Officer or the Underwriter, or is it someone else? Culminated from literally 100's of years of experience, these secrets known by only a few will enable you to gain the edge, and to keep it from start to finish. This is not to take money from the industry, but only from those who cheat, steal and lie. How do they use credit scores to get you to pay a higher rate? How they scare you with the appraisal. What is the LTV, DTI and other ratios, that they use to get you into a higher rate? How do you know if the loan has a prepay or not? How they sneak it in the back door while the customer isn't looking. Is the credit score really that important? What is "origination" anyway? And "discount"? What is a HUD-1? The Settlement or Closing statement? How to use your Escrow company effectively, on your behalf? Whose appraisal is it anyway? How to get it and get it quick? Why is my loan taking so long? What is the Funding fee? What does an underwriter do and why are they so important? Who has the final say? Why some lenders are less expensive than others? Can they really deliver? What is the APR? The EATR? How to tell if a loan officer is up and up? How to tell if they know what they are doing? How important is the processing department? The 5 top mistakes made in processing!! And how they can kill a deal. Why and how can a Loan Officer tell you whatever will make the sale and then LEGALLY get out of it? KNOW THIS ONE THING AND SAVE 25%. Customer Service

DISCLAIMER- Please Note, that I am not a financial planner. PLEASE CONSULT with a Financial Planner and/or professional, before embarking on anything gained from this site! In addition, any information is for informational purpose only. Viewer assumes ALL RISK from any information gained at this site.

|

|||||||||||||||||||||||||||||

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}